Has electricity gotten more expensive?

Yes, if you ignore inflation. Not if you look at real prices.

There is a prevalent misconception that electricity prices have risen dramatically in recent years. This is true only when inflation is ignored. In real terms, current electricity prices are about the same level as 1995-1999. Real electricity prices today are approximately where they were a decade ago, and significantly lower than their 1980s peaks. After adjusting for inflation, electricity prices peaked at about 24¢/kWh in 1985. Today, the average is about 17¢/kWh.

For about a year now, the economist Michael Giberson has pointed out this misunderstanding in response to various news reports that plotted only the nominal (i.e., not accounting for inflation) data in the graphic above. Or, news articles claiming that electricity prices have spiked without evidence.

It is difficult to overstate the importance of getting this basic fact right. Without adjusting for inflation, you aren’t making accurate or fair comparisons. These kinds of adjustments are a must. Yet, they are often forgotten.

Electricity has actually become more affordable over time, not less. This is a national average, so it washes out important variations from state policy and market design. California, for example, is significantly more expensive due to its aggressive climate policies and other policy choices. The core point is that much more than the types of electricity generators matter. It’s also about how that electricity gets to you.

Cheaper electricity, pricier wires

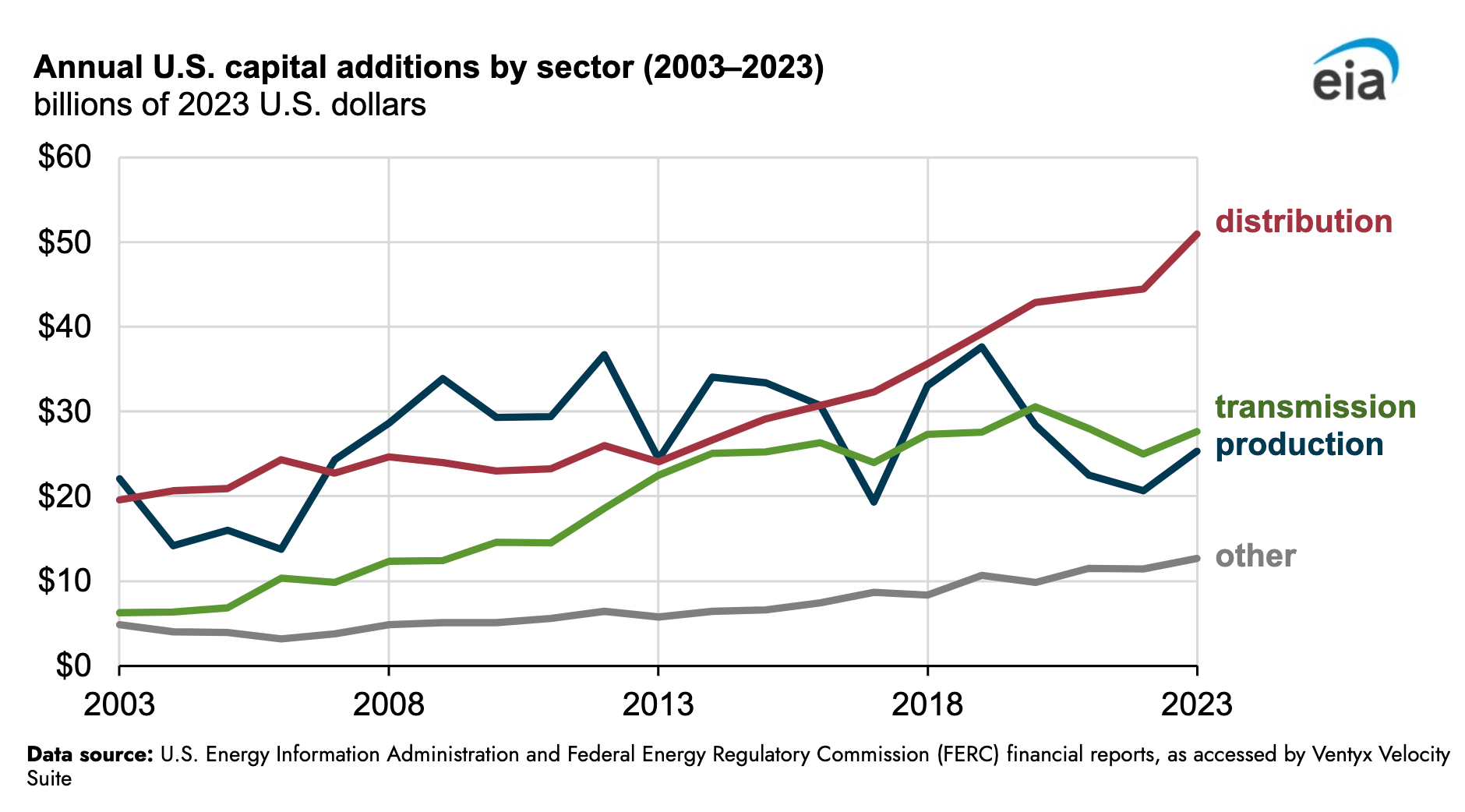

The makeup of your monthly bill has changed in ways that have less to do with fuel sources and much more to do with the maintenance of wires and poles. As Duncan Campbell summed it up in a 2022 essay, we have cheaper electricity and pricier wires.

In November 2024, the Energy Information Administration published a brief analysis that made a similar point. Grid infrastructure has accounted for an increasing share of utilities' spending over the last 20 years.

Most of this increase has been in distribution, not transmission. The EIA analysis lists transmission builds as part of the story, but a far second to distribution. This is evident in the graphic below. Transmission spending tripled, but distribution accounts for a much larger share of spending.

Where and why utilities are spending more is incredibly important for policy recommendations aimed at lowering electricity rates. A lot of debate happens on the fuel side, but that can be deceptive. Of course, fuel choices matter (and have driven up costs in some places, such as California). Renewable portfolio standards, which are state-level mandates for clean energy, can raise electricity prices.1

We should begin making electricity policy advice from the right place. This implies three facts:

Production costs have fallen.

Mechanically, lower production costs almost guarantee that transmission and distribution costs make up a growing share of the electric bill.

Consumers are paying less for electricity and more for delivery.

Don’t mess with Texas

A final point about Texas in particular. There’s an unfortunate misconception that Texas has suffered acutely from electricity price increases. This is typically associated with the significant additions of wind and solar energy in the state. It’s just not so. As Michael Giberson explained on The Energy Markets Podcast:

If you disaggregate Texas from the other states, you see a slightly more interesting story in that Texas has started about the U.S. average, for a couple of years, it was higher than the U.S. average. But since 2008 or so, 2010, it dropped below the U.S. average and spent most of the last 14 years since cheaper than the rest of the country.”

Looking at the last 20 years of Texan electricity history, there’s simply no evidence of doom and gloom from changing fuel sources.2 Texas ranked 39th in the EIA’s data on electricity costs for 2023—that makes it the 11th cheapest.

You could argue that the neighboring states, displayed in the West South Central line on the chart, show Texans pay a premium because of Texas’s free market design. However, that is belied by the long history of differences between Texas and the other states. More likely, those differences are due to fundamentals—points of difference in geography, history, or climate that are longer standing than fuel choices.

Academic reviews of Texas’s market suggest explanations like this are important. Those studies also show that residential electricity rates in Texas decline because of competition. It also demonstrates that electricity prices are more closely tied to the actual costs involved in production. That’s exactly how you want markets to spur innovations and solutions to those price changes, and it’s part of the reason traditional utility models can miss those opportunities.

A compelling reason to doubt claims that Texas has skyrocketing electricity rates is to consider where data centers and other energy-intensive industries are seeking to locate. Why would sophisticated operators want to come to Texas if rates are set to balloon? Or if the grid is about to collapse because of renewables? To be clear, this is shifting the focus to industrial rates, rather than the residential rates shown in the graphics above. However, it suggests that the biggest players in the energy world are betting on Texas’s system to provide abundant, cheap, and reliable electricity when they could choose anywhere else in the world.

The biggest players in the energy world are betting on Texas’s system to provide abundant, cheap, and reliable electricity when they could choose anywhere else in the world.

Overall, it is clear that Texas’s electricity market operates efficiently, quickly, and with a wide range of options for customers. These are incredibly valuable characteristics that other states cannot claim.

All this said, 11th cheapest doesn’t put Texas in the top ten most affordable states. And though today’s electricity prices are cheaper than those of the 1980s, they are no cheaper than in the 1990s. So there’s work left to do, some of which Duncan Campbell lays out in his essay.

Before rushing into sweeping policy changes, it is worth pausing to ensure that we have identified the correct problem. Electricity prices, once adjusted for inflation, have remained remarkably stable. Infrastructure is actually driving higher bills, not changes in fuel sources. To lower costs for consumers, we need to look beyond the power plants and into the wires.

Three further reading recommendations:

This shouldn’t be surprising, but sometimes I get pushback here. These policies tell utilities to make purchases and build regardless of price. Given their designs, it would be a wonder if they didn’t raise prices. A utility representative once told me that he did not care about clean energy mandates because he could just ratebase the costs! At the same time, the reductions in electricity production spending in the above charts demonstrate the effects that additional competition can bring to electricity markets.

For more on this, Brendan Pierpoint at Energy Innovation published a useful paper in July 2024. One quibble with it is that the paper does not consider RPS costs in the detail they deserve, given the strong theoretical reasons to expect price increases from mandates. To be fair, such clean energy mandates are only one policy of many.

What is the difference between “distribution” and “transmission?” Can you give some examples of each?

Dr. Gale Pooley, co-author of Superabundance, has the following substack on the price of KWH. https://newsletter.humanprogress.org/p/the-declining-time-price-of-kilowatt?r=2i0kgv&utm_campaign=post&utm_medium=web