ERCOT is the only one getting energy-only right

Texas embraces dynamism against stasis

If you and I want to build a new generator and sell the electricity, then we’ll have to connect to the wires that carry our generation out to consumers. Doing that requires an interconnection approval. The exact process for that differs everywhere, and only the broad strokes are relevant to the point at hand today.

When you and I want to connect, there are two lines for us to choose from:

Energy resource (ERIS), or

Network resource (NRIS).

Before we go any further, here’s the punchline: Only ERCOT is getting energy resource processes right. If you take that away, then you don’t need to read further.

For a quick and dirty understanding, energy resource connections allow generators just to sell electricity in the market. They are simply merchants selling electricity. In contrast, a networked resource is eligible for the administrative capacity programs. Networked resources can sell electricity in the market and bid into reserve programs for tight moments on the grid, which includes its own remuneration even if the generators don’t run. I covered the differences and why this matters in two earlier pieces.

Why it matters that Texas is the fastest runner

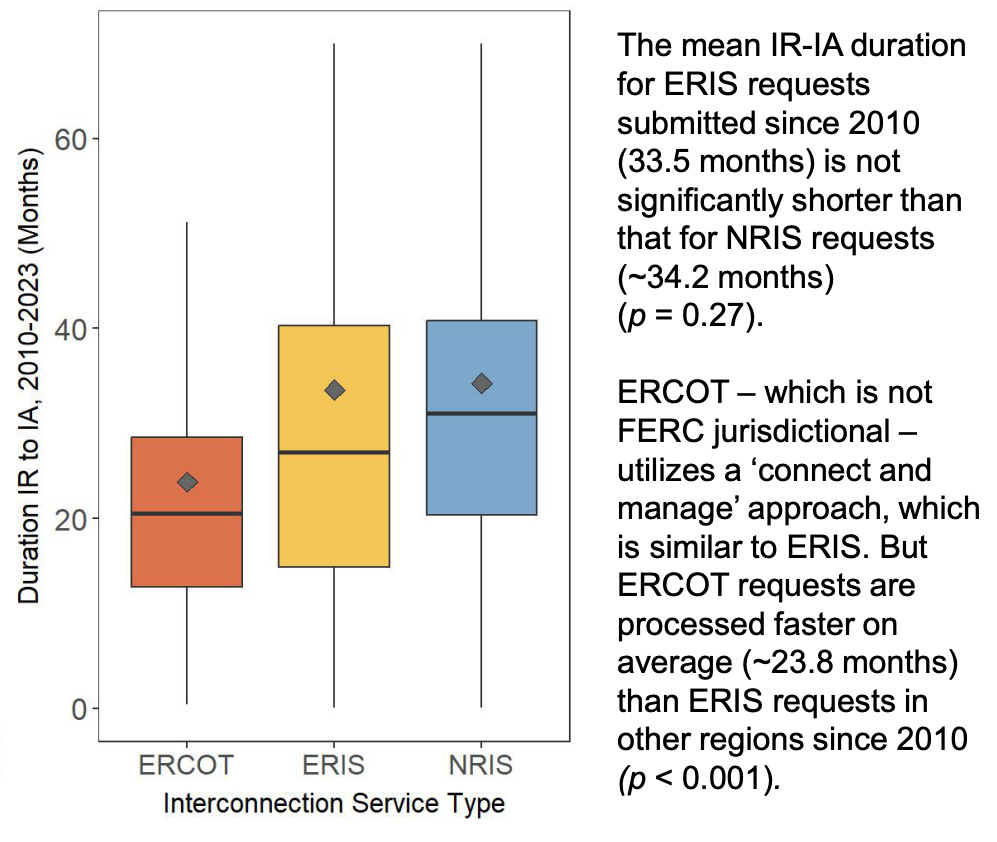

Part of ERCOT’s secret is pushing everyone into the same line to register as an energy resource. In Texas, there is only the option to connect as an energy resource. Texas runs an energy-only system. If you and I want to connect our new generator in ERCOT, then we only have one choice–the ERIS line. That secret sauce connects everyone almost a year faster than everyone else–23.8 months compared to 34.2 months.

This graphic from the Lawrence Berkeley National Laboratory’s 2024 Queued Up report shows just how much faster and more certain Texas makes interconnection. Everywhere else, the two lines take just as long. That’s shown in the blue and yellow boxes in the plot below. The ERIS and NRIS lines are equally long. ERCOT, in the orange, is faster than both NRIS and ERIS processes elsewhere.

What’s important from this graphic for the rest of the country is that the average energy resource line is not a fast lane. It takes just as much time as a networked resource. That’s a problem because it slows down the addition of generators that could provide electricity during moments of high prices.

There’s not just a benefit then of speed in ERCOT, but much more certainty. Remember, the whiskers on the box plots show the spread of the interconnection timeline. To be technical, the whiskers show “1.5 times the [interquartile range].” ERCOT’s shorter whiskers represent that Texas gives entrepreneurs fewer hoops and a clearer runway.

That ERCOT is faster at connecting resources is vital for reducing energy costs. If you want customers to be served quickly, then you need to quickly connect energy resources. Said another way, if you want entrepreneurs to bring down high energy prices, then ERCOT is the right model. ERCOT has the fastest system.

Three e’s of progress (and electricity): Experiment, evaluate, evolve

I am planning a longer entry on this idea, but it may help clarify why this faster process matters. Economist Arnold Kling sets an aphorism up for understanding progress, “Progress comes via the three e’s: experimentation, evaluation, and evolution. It does not come via intelligent design.”

Because Texas encourages experimentation in its energy-only system, actors within the market learn more, learn faster, and can evolve the system. Consider battery storage in Texas as an example. Batteries are a massive portion of what is coming online in Texas soon. About 147GW are sitting in the state’s interconnection queue as of July 2024. If we just look at what is planned for the next two years, 2024 and 2025, we should see almost 50GW of storage join the ERCOT market. In 2026, more than 50GW is planned. Not all of this is guaranteed, of course, and significant portions of the queue will not make it to the grid.

The important point here is to think about the Texas energy ecosystem. Though there are extensive federal support programs for batteries, no state-level requirement or mandate exists. To use Kling’s phrase, no intelligent designer made a call to put 147GW of batteries in the queue. Nor did any central planner like a utility decide to go big on batteries. Instead, hundreds of entrepreneurs saw opportunities, experimented, evaluated how their investments fared, and evolved their strategy for the next round of play. That’s an enviable dynamism that exists only in Texas.

The rest of the country’s grid operators have something to learn from Texas. The primary lesson is the way that Texsa enables faster experimentation, evaluation, and evolution on the grid. That’s becoming more important every day as queues grow and concerns about meeting the needs of data center companies arise.

Texas’s energy-only system is a strong contender to lead the way through the challenges of building to meet the needs of our prosperous future.

More reading on Texas and connect and manage

If you want more on connect and manage, or the Texas approach relative to other places:

Beyond FERC Order 2023: Considerations on Deep Interconnection Reform, Tyler Norris.

Generator Interconnection, Network Expansion, and Energy Transition, Jacob Mays.

Electricity Restructuring: The Texas Story, Andrew N. Kleit and Lynne Kiesling.

Queued Up, this NREL annual report has just started breaking out ERCOT to look at the connect and manage system relative to the rest of the country.